The Two Emerging Players on M&A’s Main Street

8 minute read

Middle-market M&A has traditionally been dominated by two main players: the strategic buyer and the financial buyer, typically a private equity group. In recent years however, the financial buyer landscape has evolved with two new players emerging: the family office and the independent sponsor.

Private Equity Recap

If you happen to live outside of the M&A world, your initial impression of ‘private equity’ may be derived from movies like Wall Street with Michael Douglas as Gordon Gekko or Pretty Woman with Richard Gere – emotionless gamblers playing high stakes games of financial poker with the lives of the average working man in the balance. Anti-heroes uttering memorable lines like, “I am not a destroyer of companies, I am a liberator of them,” (Gekko); and “I don’t sell the whole company, I break it up into pieces, and sell them off because it’s worth more than the whole” (Gere).

Private equity’s bad reputation dates back to the 1980’s junk bond era and the classic Hollywood movies and actors that have glamorized the so-called “greed is good” pure capitalist mentality.

BUT, yesterday’s private equity looks nothing like today’s. TODAY, Private equity focuses on growth, both organic and inorganic. Private equity groups are operating companies themselves. They offer a service with a focus on achieving a great rate of return for their investors, their fund, and their portfolio companies. Their fundamental objective is to buy businesses and then transform them to larger and more profitable entities. Additionally, private equity is now the second largest employer1 in the US making this asset class a valuable component to our economy.

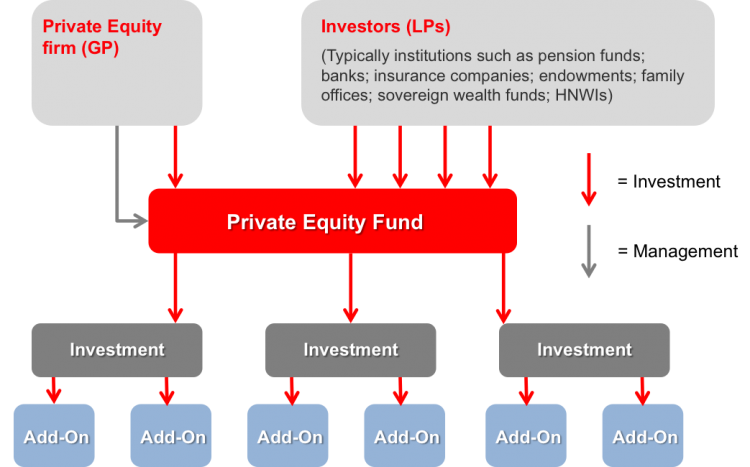

The Anatomy of a Private Equity Fund

Limited Partners (“LPs”) are the principal investors in a private equity fund, which is managed by a General Partner (“GP”). GP is also referred to as the private equity firm.

GPs raise an investment fund from investments made by LPs. LPs have an expectation for a certain return on their investment that the GPs have targeted. Additionally, as part of their subscription, the LPs agree to pay a management fee to the GPs.

The private equity fund’s lifecycle is typically 10 years. GPs must deploy their funds over this period of time and achieve their expected rate of return.

The way a GP sets about generating returns involves a deployment of its funds to purchase a ‘platform company’, a company large enough to scale, grow organically (implement operational efficiencies, employ resources, provide support and sales), and ‘bolt-on’ or ‘add-on’ synergistic companies. This approach is known as the ‘buy-and-build’ strategy. The ‘buy-and-build’ strategy is a commonly employed private equity methodology utilized to gain market share and increase corporate earnings.

Family Office Recap

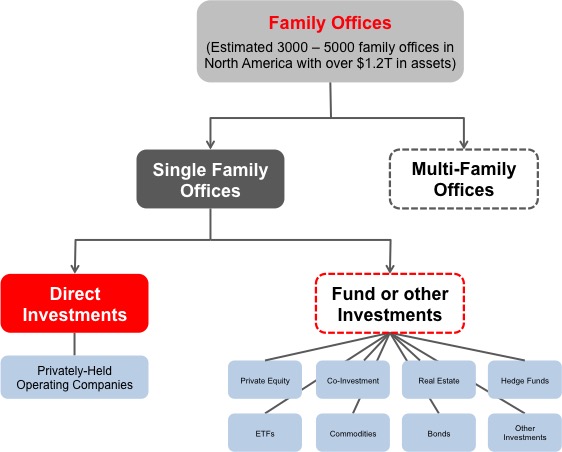

The family office, in particular the single family office (“SFO”), is a private company that manages investments and trusts for a single, ultra high net worth family2. The financial capital of the company comes from the family’s wealth, which typically originates from the successes of earlier family business ventures and is an accumulation over several family generations. These families often have deep knowledge and expertise in the industries from which they derived their wealth.

The objective for the SFO is to deliver investment returns to the family in addition to other services that include: property management, day-to-day accounting and payroll activities, management of legal affairs, family governance, financial and investment education, philanthropy coordination, and succession planning3.

There are believed to be over 3,000 family offices in North America, and these family offices control over $1.2 trillion in assets4. These assets include: private equity, real estate, hedge funds, ETFs, bonds, direct investments, among many others.

The Anatomy of a Family Office

Opportunities emerge for the family office: More control and higher returns

Traditionally, the family office has taken a passive role as a limited partner in a private equity fund when investing in middle-market companies. The private equity fund has proven to be an attractive investment asset class for family offices, with private equity-backed middle-market companies outperforming the S&P 500 by 400 – 600 basis points from 2013 – 2016, according to the Golub Capital Altman Index.

However, over the past few years there have been concerns about transparency around fees and fee disclosure5. Additionally, as family offices become more sophisticated in managing their own investments, they are deliberately pursuing direct investments in middle-market companies sans the private equity fund.

The advantages for family offices executing their own direct investments include:

- More control – Family offices are no longer required to park their capital in a fund for its 10-year holding period. Also, the family office now has the ability to make decisions concerning their investments. As an LP in a private equity fund, the family office had ‘limited’ say in the GPs investment management.

- Higher returns – Family offices no longer have to share their earnings with the GP. Moreover, from an expense viewpoint, family offices no longer have to pay those hefty management fees.

The Rise of the Independent Sponsor

Recently there has been a surge of a brand new type of buyer – the independent sponsor, sometimes referred to as the fundless sponsor. An independent sponsor is an M&A professional with the objective to buy and transform a business or businesses without having a dedicated fund like a private equity group or the wealth to draw from like a family office. Essentially, as the name suggests, they are ‘fundless’ and seek capital (investors) when consummating a deal.

With the current capital markets landscape, there is a disproportionate amount of capital looking to invest in the limited number of private companies coming to market. Independent sponsors locate these companies even before having the committed capital. Once these independent sponsors locate an acquisition target, they will oftentimes make an offer to buy the company, putting that company under an exclusivity period, typically 60 days, during which time that company cannot engage with any other potential acquirers. The independent sponsor thereafter reaches out to its network of private equity funds, mezzanine funds, family offices, and other investors to raise the money to acquire the company.

Unfortunately, the independent sponsors are not always successful with the capital raise, and consequently tie up the company’s owners in a lengthy exclusivity period delaying the sale of their business. However, there are several independent sponsors that are highly experienced, highly successful M&A professionals.

Family offices and other investors have grown to appreciate the independent sponsor. For family offices, the independent sponsor provides the benefits of a private equity fund in addition to offering the flexibility of investing on a case-by-case basis as opposed to a 10-year investment commitment. Additionally, independent sponsors do not require a management fee, and the family office has more input into managing the investment.

Beware of the Bad Actors

There are very few barriers to entry for an independent sponsor. In fact, the top business schools train their students on how to become an independent sponsor right out of school with little to no experience.

In conjunction with the robust capital markets, there has been a significant rise of individuals proclaiming they are independent sponsors. They look and sound like they are a private equity fund or a family office, but they lack both the capital and the experience. These ‘bad actors’ may not have the ability at all to consummate an M&A transaction, yet they are out in the market speaking directly to business owners, and moreover, they are placing offers on businesses, sometimes making unrealistic offers which distract the owners from more credible offers. These ‘bad actors’ may lack the access to capital altogether and are consequently unsuccessful in the capital raise, which delays the company’s sale. This creates a great deal of frustration and confusion for the business owner; hence the importance of having a trusted and experienced M&A advisor. This advisor should have a good understanding of which buyers are real, motivated, and most likely to consummate a transaction.

New opportunities for the business owner

With the rise of family offices and independent sponsors, this presents new opportunities for the business owner. Business owners now have two additional types of buyers competing for the purchase of or investment in their companies. A good investment banker utilizes these new buyers as well as the more traditional players to create an auction environment that generates multiple offers ultimately resulting in the best outcome for the business owner. With the rise of these new buyers, a good banker will draw upon their personal experience and the institutional knowledge of their firm to assess the buyers involved and the quality of their offers.

Additionally, between today’s private equity, family offices, and independent sponsors, the business owner’s legacy remains intact. Because the buyers of today have a central focus on growth, the business owner can even expect an expansion of their legacy. Yesterday’s Gordon Gekkos and Edward Lewises (Gere) are just a vanishing fragment of M&A’s history.

Related articles by Allegiance Capital:

Sources:

- Chiu, Marcus. “Private Equity, an Employer of Millions, Turns its Attention to Talent.” Gartner. Web. 13 Sept. 2017.

- Douglas, Craig; Todd Wollack. “Case highlights family office risk.” Boston Business Journal. Print. 27 Jun. 2007.

- Beyer, Charlotte B. “Family Offices in America – Why the Bloom is off the Rose.” The Journal of Private Portfolio Management. Fall 1999.

- Sankaran, Ameeth. “Is family office “patient capital” more helpful than Venture/PE funding?.” Medium. Web. 14 Jul. 2016.

- Staff Writer. “Private Equity’s Other Transparency Problem.” Institutional Investor. Web. 8 Jul. 2017.

Photo by rawpixel.com on Unsplash