The 3-Ingredient Recipe for a Ripe Exit

7 minute read

Today, all of the signs suggest we are in the midst of an inflection point in the M&A market. Currently, there are three main elements, or ingredients, that have transpired in today’s market and have positioned privately-held companies and their shareholders to yield extremely favorable returns if a liquidity event, or sale of their company is actualized. Those ingredients include: 1) the capital markets, 2) the current market cycle, and 3) the great wealth transfer.

The Capital Markets

We are currently in the second longest bull market in history. As of March 9, 2018, the bull market reached its 9th birthday. High valuations, record low interest rates, and the amount of capital in the markets can all be attributed to this bull market. The longest bull market was 9 years and 7 months old (115 months) beginning in 1990 and ending in the dot-com bubble.

Moreover, there is an astounding amount of investible capital driving the activity in the M&A markets. There is approximately $2.9 trillion of capital sitting on the sidelines today to either buy or invest in successful, middle-market companies. Of the $2.9 trillion of investible capital, $1.9 trillion is in the form of cash on corporate balance sheets,1 and the other $963 billion is dry powder (earmarked capital for investment) held by private equity.2

What’s not accounted for in these figures is the amount of capital designated for direct, private company investing from family offices. There are believed to be over 3,000 family offices in North America who control over $1.2 trillion in assets, and it is unknown as to the amount they have dedicated to direct private company investing.3

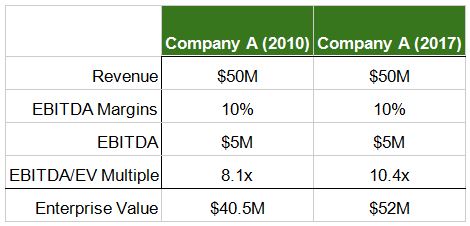

Now, let’s discuss the market’s record high valuations. At the end of 2017, the median M&A multiple for all M&A transactions was 10.4 times EBITDA to Enterprise Value, according to Pitchbook. In 2010, during the early stages of the business cycle’s expansion phase, the median M&A multiple for all transactions was approximately 8 times EBITDA to Enterprise Value. That is nearly 2 and a half additional turns of appraisement! See the computative example below:

Figure 1.0: EBITDA to Enterprise Value Calculation (2010 vs. 2017)

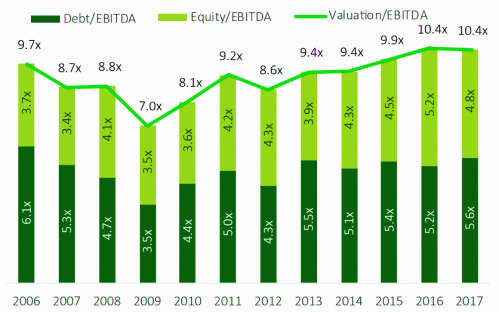

Figure 2.0: Median valuation to EBITDA in M&A deals has grown in each of the past four years

Source: Pitchbook

Additionally, what’s also driving up valuations are the debt markets and low interest rate environment. In short, money is still very cheap. A great illustration of the effect of interest rates and market valuation can be seen in an article by Chase Hinderstein from The Wise Investor Group. Essentially, it illustrates that one dollar earned next year, or even five years from now, is worth more to an investor today than at almost any time in history. One dollar of earnings next year is worth almost one dollar to an investor today. However, if the interest rate of those future earnings were to increase, then next year’s dollar of earnings may only be worth $0.94 to an investor today. In this case, investors would not be willing to pay the premiums they are paying today for private companies.4

Cycles & Market Swings

In life, timing is everything, and it is no different in the M&A market. The M&A market, like seasons, goes through its cycles. On one end of the spectrum is a ‘seller’s market’ and on the other end of the spectrum is a ‘buyer’s market’.

Furthermore, deal market cycles are extremely important for business owners to keep in mind when considering an exit strategy or liquidity event, but they are often overlooked or the business owner may be uninformed. The supply-demand balance for buyers and sellers, the availability of debt to finance transactions, and the overall economy are all major factors when considering a private company sale. As stated by veteran M&A professional and author Robert T. Slee, “Deal periods in a transfer cycle are not binary switches. Rather, they are like leaky deal faucets. There are opportunities in every period […]. However, sellers are more likely to get a good deal in a seller’s market.”5

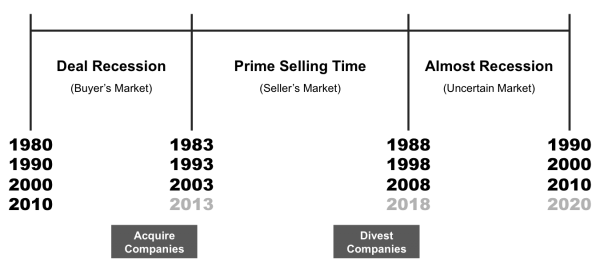

Figure 3.0: The United States Ten Year Private Transfer Cycle

Source: Slee, Robert T. Private Capital Markets, Valuation, Capitalization, and Transfer of Private Business Interests. Publication. 31 May 2011.

Today we are in a seller’s market, which means there is a higher demand for businesses for sale because of an excess supply of capital that needs to be invested – more dollars are chasing fewer deals. This results in higher valuations for the seller. Ideally, a business owner should look to maximize his or her exit with strategic timing – selling in a more favorable market. As discussed in this article, there has never been such a high magnitude of pro-seller events converging all at once.

Based on the deal market cycles as shown in Figure 3.0, we may be entering a buyer’s market in the near future. A buyer’s market means there is a higher demand for investment capital because of supply – there are more businesses in pursuit of a limited amount of capital. In this type of market, buyers have the weight of the leverage and possess the power to buy at lower valuations.

Whether the current market is a ‘seller’s market’ or a ‘buyer’s market’, demand can be generated by experienced investment bankers. To learn more about market creation and generating demand for private companies, see our article on the subject here.

The Great Wealth Transfer

Baby Boomers, the wealthiest generation in U.S. history, will pass down an estimated $30 trillion in assets to their children and grandchildren.6 These assets consist of both financial and non-financial assets, and more specifically for some, these assets consist of their business interests. Furthermore, Baby Boomers equate for 43% of small business ownership (businesses under 50 employees), which is an estimated 12,000,000 businesses.7

As Baby Boomers began to retire in 2011, they started divesting their business interests. As a greater number of baby boomer owned businesses enter the market, there will be a shift towards a buyer’s market as there will be more businesses seeking a limited amount of capital.

Ripe Time for Exits – The Window for Ideal Returns

As mentioned in the opening of this article, the activity in the M&A market today suggests we are in the midst of an inflection point. The key three ingredients – the capital markets, the current market cycle, and the great wealth transfer – project a yield of extremely favorable returns for business shareholders inside the market’s current window. Due to the current levels of GDP growth, unemployment rate decline, wage growth, and inflation fears, a rise in interest rates is imminent, which means investors will not be willing to pay the premiums they are paying today for businesses. Additionally, the expected flood of businesses coming to market from retiring Baby Boomers emphasizes the importance of strategic exits. If a business owner is on the fence about “taking chips off of the table”, he or she may want to reconsider as it could be another 7-10 years before the markets are in his or her favor again.

Related articles by Allegiance Capital:

- How to know when the ride is over and it’s time to get off

- When Selling Your Company May Actually Make Sense

- Getting Deals Done – Generating Demand vs. Supply

- The Two Emerging Players on M&A’s Main Street

Sources:

- Global Credit Research. “Moody’s: U.S. corporate cash pile to rise 5% to $1.9 trillion in 2017; tech sector dominates again.” Moody’s. Print. 20 Nov. 2017.

- Mittelman, Melissa. “Why Private Equity Has $963 Billion in Dry Powder.” Bloomberg. Web. 31 Aug. 2017.\

- Sankaran, Ameeth. “Is family office ‘patient capital’ more helpful than Venture/PE funding?.” Medium. Web. 14 Jul. 2016.

- Hinderstein, Chase. “The Effect of Interest Rates on Market Valuation.” The Wise Investor Group. Web. Retrieved 18 Mar. 2018.

- Slee, Robert T. Private Capital Markets, Valuation, Capitalization, and Transfer of Private Business Interests. Publication. 31 May 2011.

- Robaton, Anna. “Preparing for the $30 Trillion Great Wealth Transfer.” CNBC. Web. 30 Nov. 2016.

- Cuneo, Chris. “The Numbers Don’t Lie.” Lindquist & Vennum LLP. Print. 12 Jul. 2016.

Photo by Brooke Lark on Unsplash